Can You Go to Jail for Selling a Car With a Lien?

Selling a car you still owe money on can feel risky. You might worry about criminal charges or jail time in case you sell the car without telling the buyer a lien exists. The good news is that in …

Selling a car you still owe money on can feel risky. You might worry about criminal charges or jail time in case you sell the car without telling the buyer a lien exists. The good news is that in …

Adding a spouse to your car title after getting married? Trying to remove an ex after a divorce? When your car has a loan, the process requires an extra step. This guide covers how to add or remove a …

A lien is a legal claim someone can place on your car that allows them to take or sell the vehicle until a debt is fully paid. Sometimes this can happen without you even knowing. Can a Lien Be …

Whether you’re buying or selling a used car, confirming a loan payoff, or trying to avoid lien scams, this guide shows you how to check for liens quickly and for free. A lien is a legal claim on a …

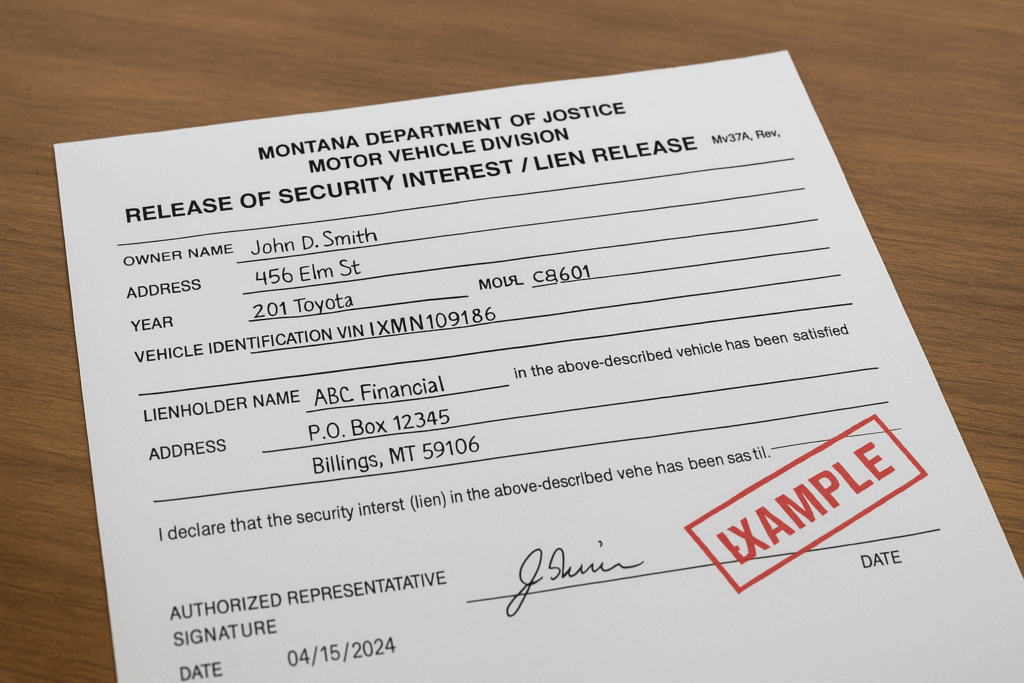

Just paid off your title loan? Good news: you most likely do not need to do anything. In most cases, getting a lien release after fully paying off your title loan is completely automatic. Your title loan company removes …

A lien is a legal claim that protects the lender until a debt is paid. Can You Put a Lien on a Car as an Individual? Yes, you can. You don’t need to be a bank or finance company. …

Removing a lien means getting a clean title that proves you own the vehicle free and clear, with no lender claims against it. What You Need to Know About Removing a Lien Once you pay off your car loan, …

What Is a Second Chance Loan? A second chance loan isn’t just one specific loan. It’s a group of lending options created for people with bad credit or past financial challenges. If you’ve been denied by a bank but …