Home Refinance Title Loan

Refinance Title Loan

Published on

Fact-Checked

Close

Each article is reviewed by our editorial team and fact-checked for accuracy using credible sources. We regularly update content to reflect current information (see last update at top of article). Learn more about our editorial standards.

How much cash can i get

Find out now. It's fast, secure & free!

Car title loans can provide fast cash, but they often come with a very high interest rate and service issues may lead to regrets about your lender choice. Are you looking to reduce your title loan payments or in need of additional funds? Well, it’s not too late. Making informed personal finance decisions is crucial when considering refinancing.

Montana Capital is here to assist!

We offer car title loan refinance programs for cars, motorcycles, RVs, and more, aiming to decrease your monthly payments and provide the extra cash you might need.

If you’re wondering, “can I get more money on my title loan?” refinancing may be the answer. Depending on your vehicle’s equity and loan terms, you might qualify for additional funds while lowering your monthly payments.

Our approach is straightforward and designed for your convenience, with a history of assisting thousands in improving their title loan terms and helping them secure more favorable loan terms.

Montana Capital Title Loans Refinancing

Considering a refinance? The refinancing process begins with a simple loan application. Reach out to us for a no-obligation, free estimate and discover if refinancing your car title loan is the right move for you.

It’s an opportunity to save a lot of money and discover more competitive interest rates without any risk.

Key Takeaways

- Refinancing a title loan means replacing your existing car title loan with a new loan that offers better terms, such as lower interest rates or reduced monthly payments.

- The refinance process involves applying with a new lender or your current lender, who pays off your old loan and issues a new loan agreement.

- You may qualify for refinancing even if your vehicle is not fully paid off, as long as you meet the lender’s requirements.

- Refinancing can provide access to extra money if your vehicle’s equity exceeds the amount owed on your current loan.

- Benefits of refinancing include avoiding defaulting on your current loan, lowering monthly payments, extending repayment periods, and potentially improving your credit score through timely payments.

- Be aware of possible fees such as origination fees, prepayment penalties, and title transfer fees that can affect your savings.

- Gather necessary documents before applying, including proof of income, vehicle title, government-issued ID, and current loan details.

- Refinancing can be a useful tool to manage high-interest, short-term car title loans and improve your overall financial situation.

In a Nutshell: What Does it Mean to Refinance a Title Loan?

Refinancing your car title loan means obtaining a new loan to replace the existing one, potentially with better repayment terms such as reduced monthly payments or lower interest rates.

Refinancing can also help you achieve lower monthly payments by extending the loan term or securing a lower interest rate, making it easier to manage your finances.

This option is available whether you wish to continue with your current lender or switch to a new one for better terms. Auto title loan refinance is similar to refinancing a car loan or auto loan, but it may have different requirements and paperwork involved.

What is a Car Title Loan?

A car title loan, sometimes called an auto title loan, is a type of short term loan that lets you borrow money using your vehicle’s title as collateral. With a car title loan, you hand over your car title to the lender in exchange for a cash loan, while still being able to drive your car during the repayment period. The lender becomes the lienholder on your car title until the loan is fully paid off.

Title loans are popular for their fast approval process and minimal credit requirements, making them an option for people who need quick cash and may not qualify for traditional loans. However, car title loans often come with very high interest rates and fees, which can make them an expensive way to borrow money. If you’re unable to repay the loan as agreed, the lender has the right to repossess your vehicle to recover their losses.

Because of the risks and costs involved, it’s important to fully understand the terms of any car title loan or auto title loan before signing the loan agreement. Always compare interest rates, loan terms, and fees from different title loan lenders to ensure you’re making the best financial decision for your situation.

Our Title Loan Refinance Process is Simple!

- Fill out and submit the online form or contact us at 800-700-8900.

- Provide your current loan details to one of our loan officers.

- Our loan officer will illustrate potential monthly savings through refinancing.

- Submit all required documents and items requested by the loan officer.

*You may also need to provide your bank account information for direct deposit of any extra funds from your refinanced loan. - Start enjoying reduced payments after completing the process.

Timely payments on your refinanced loan can be reported to credit bureaus, which may help improve your credit profile.

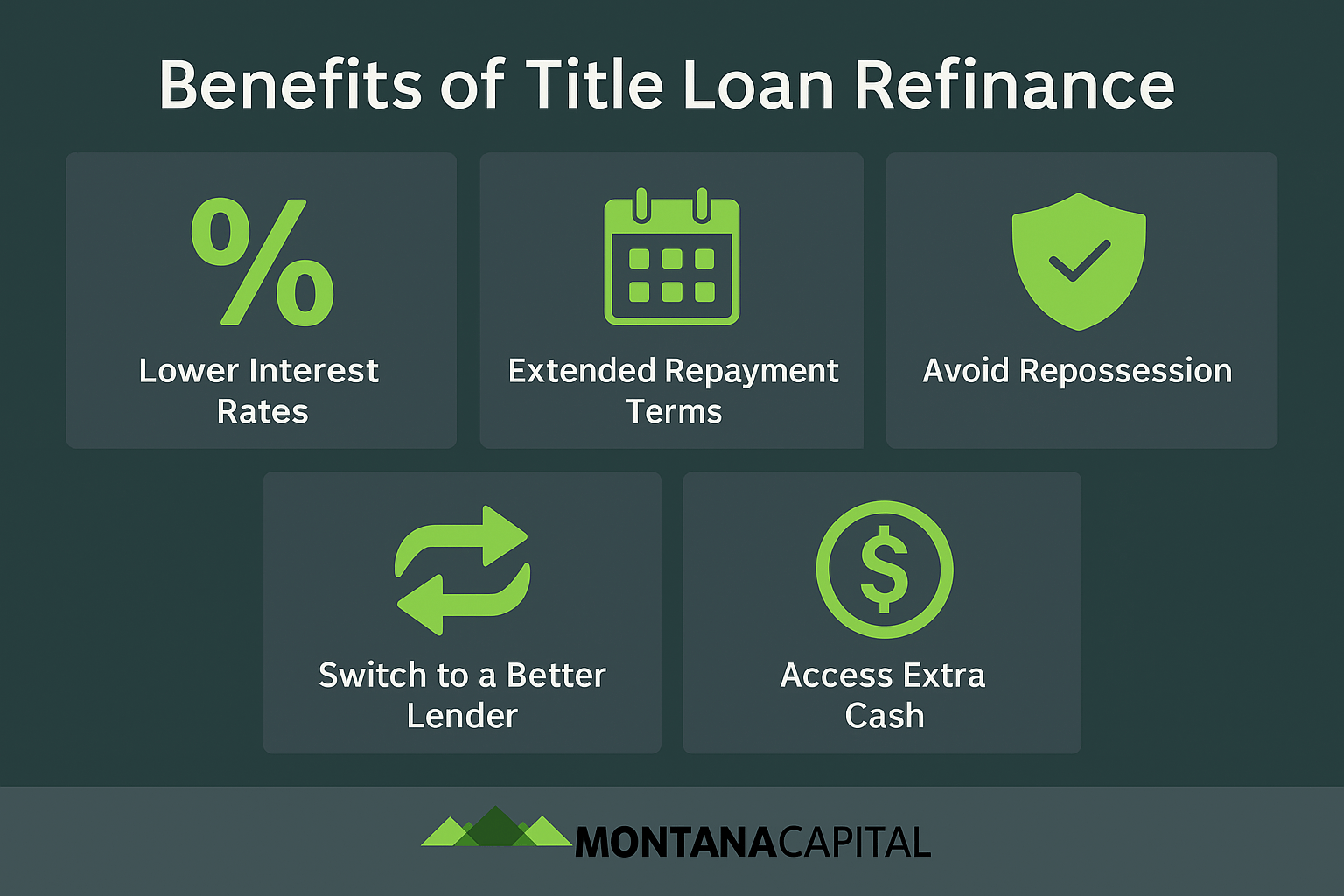

Benefits of Title Loan Refinance

- Lower Interest Rate: Refinancing your auto title loan can lead to reduced interest rates, keeping more money in your pocket over the loan’s duration.

- Extended Terms: Refinancing may allow for longer repayment periods, easing the burden of high monthly payments.

- Avoid Repossession: Refinancing can help prevent vehicle repossession by offering more manageable payment plans.

- Switching Lenders: Refinancing your car title loan allows you to switch to a lender with better customer service, improving your overall experience.

- Access to Additional Cash: Depending on your vehicle’s equity and the refinance terms, you might access extra funds while still lowering your overall monthly payments.

Required Documentation For Title Loan Refinance

Before delving into the refinancing process, some preparation is required.

The required paperwork for refinancing will resemble the documents you submitted when applying for your current car title loan.

- Proof of Income: Submit recent paychecks or bank statements as evidence of your steady income, which is crucial for securing the terms of your new loan.

- Vehicle Title: Provide the original title of your car, ensuring it’s free of liens, or include a lien release if the car is still under financing.

- Government-Issued ID: Have on hand a valid driver’s license, passport, or any official state identification to verify your identity.

- Proof of Residence: Show a utility bill or your lease agreement to confirm your current living address.

- Current Loan Documentation: Offer details about your current car title loan, such as the loan amount and your lender’s contact information.

- Vehicle Registration: Ensure your vehicle’s registration is current and valid for the car associated with the title loan.

- Insurance Information: Demonstrate proof of either comprehensive or liability insurance coverage for your vehicle.

How to Refinance Your Title Loan?

Title loan refinancing is a straightforward process, similar to applying for a new auto title loan. However, before you begin the application, there are some important steps to take.

Steps to Prepare for Title Loan Refinancing:

1. Review Your Current Contract

Take the time to thoroughly examine your existing title loan contract.

Ensure that your title loan lender is adhering to the terms and conditions, and check for any clauses that may complicate refinancing, such as early termination fees.

2. Qualifying for Refinancing

Refinancing doesn’t automatically guarantee a better deal. You must qualify first, demonstrating your ability to repay. Issues like defaults and late payments may affect your eligibility.

Be sure to review the loan requirements thoroughly to avoid disqualification.

3. Explore Your Options

Montana Capital Car Title Loans is one of the leading auto title loans providers in southern California, offering unique options that set us apart from others.

Take the time to explore the various loan options available, including our competitive rates calculated using our loan calculator. If you have any questions, don’t hesitate to reach out to us for assistance.

4. Determine Your Loan Amount

Consider whether you need to adjust your loan amount when refinancing.

Depending on your repayment progress, you may have the opportunity to borrow more or less than your initial loan amount.

5. Apply for Refinancing

Once you’ve addressed these considerations, you’re ready to start the application process.

Be prepared to provide necessary documents and information, and don’t hesitate to reach out if you have any further questions or concerns.

Remark: By following these steps, you’ll be well-equipped to pursue title loan refinancing and make informed decisions about your financial situation.

Various Payment Alternatives

The new title loan lender will discuss various repayment options with you. Our company provides the following methods to repay your new title loan:

- Set Up Automatic Payments

- Mail Checks

- Online Portal Payment

- Phone Payments

- In-Person Payments at Nearby Locations

Hidden Fees and Charges

When considering title loan refinancing, it’s crucial to look beyond just the advertised interest rate and monthly payments. Some car title loan lenders may include hidden fees and charges in the new loan that can increase your overall costs. Common fees to watch out for include:

- Prepayment penalties: fees charged for paying off your loan early.

- Origination fees: charges for processing your new loan.

- Late payment fees: penalties for missed payments.

- Document preparation fees: costs related to loan paperwork.

- Title transfer fees: expenses for transferring the vehicle title to the new lender.

These extra costs can add up quickly and make your refinanced loan more expensive than expected. Before agreeing to any new loan, carefully review the loan agreement and ask your lender to explain any fees you don’t understand. It’s also a good idea to check your credit report for any errors or issues that could impact your ability to refinance at a lower interest rate.

By staying informed and asking the right questions, you can avoid hidden fees and secure a refinancing option that truly lowers your monthly payments and helps you save money over the life of your loan. Always make sure you understand every aspect of your new loan before signing, so you can enjoy the benefits of lower interest rates and more manageable monthly payments without any surprises.

Refinancing a Car Title Loan in California

Refinancing a car title loan in California offers individuals an opportunity to enhance their financial standing.

By renegotiating loan terms, borrowers can aim for lower interest rates or longer repayment periods. Additionally, they may tap into extra funds based on their vehicle’s equity.

Partnering with a trustworthy lender like us allows Californians to navigate tailored refinancing options. This partnership provides a pathway to improved financial management and relief from existing burdens.

Lender Tip: Only consider refinancing your car title loan if the new loan provides improved terms and rates compared to your current one. Otherwise, it might not be beneficial.

Is it a Good Idea to Refinance a Title Loan?

Refinancing a title loan can be a smart choice if it lowers your interest rate, reduces your monthly payments, or gives you access to extra cash. It can also help you avoid defaulting on your current loan and prevent vehicle repossession by making payments more manageable.

However, make sure the new loan offers better terms than your existing one to truly benefit from refinancing.

Comparing Refinancing with Other Debt Relief Options

| Option | How It Works | Benefits | Considerations |

| Refinancing | Replace your current title loan with a new loan with better terms. | Lower interest rates, reduced monthly payments, longer repayment periods, possible extra cash. | May involve fees; can extend repayment period, increasing total interest paid. |

| Negotiating with Lender | Work directly with your lender to adjust payment terms. | Potential fee reductions, temporary payment relief. | Depends on lender cooperation; loan terms usually remain unchanged. |

| Credit Counseling | Get professional help to manage debts and budgeting. | Support in organizing payments and financial planning. | Does not alter loan terms; requires commitment to plan. |

| Debt Consolidation | Take a personal loan to pay off title loan and other debts. | Simplified payments, potentially lower interest rates. | Requires good credit and income; may not be accessible to all borrowers. |

Choosing the right option depends on your credit history, income, vehicle value, and financial goals. Evaluate each carefully to find the best fit for your situation.

FAQs

Do You Get More Money When You Refinance a Title Loan?

Yes, you might obtain extra funds during the refinance process if your vehicle’s value exceeds the loan balance.

When You Refinance a Car Who Gets The Title?

When you refinance a car, the new lender typically becomes the lienholder on the vehicle. This means that they hold the title until the loan is fully paid off.

Once the loan is repaid, the title is transferred back to you, the owner of the car.

What Qualifies You To Refinance Your Car?

To qualify for refinancing your car, several factors are typically considered by lenders:

- Good credit score

- Sufficient equity in the car

- Stable income

- Age of the existing loan

What Are The Requirements to Refinance a Car Title Loan?

- Clear Title: You must own the vehicle outright.

- Sufficient Equity: The car should have enough equity.

- Proof of Income: Lenders may require income verification.

Do I Need Good Credit to Refinance a Car Title Loan?

No, having good credit isn’t necessary to refinance a car title loan. Title loan lenders primarily consider your vehicle’s value and your income when approving car title loan refinancing.

However, they may still take your credit history into account.

What’s The Difference Between Title Loan Buyout and Title Loan Refinance?

While both title loan buyout and title loan refinance involve replacing a current title loan with a new one, there are distinct differences between the two.

Title Loan Buyout: This occurs when a new lender pays off your existing title loan and provides you with a new loan agreement.

The primary goal is to offer you better terms or lower interest rates. Essentially, you’re switching companies, and the new lender takes over the lien on your vehicle.

Title Loan Refinance: Refinancing, on the other hand, can happen with the same lender or a new one. It typically involves renegotiating the terms of your current title loan agreement to secure more favorable conditions.

The focus here is on modifying your current loan’s terms rather than starting a new with a different lender.

Get More Cash and Lower Monthly Payments with Title Loan Refinancing

Need to make your car title loan payments more manageable? Wondering, “can I get more money on my title loan?” Refinancing may provide the extra cash you need while lowering your monthly payments, depending on your vehicle’s equity and loan terms.

Our car title loan refinance service is designed to help. With our easy process and history of helping many customers, we make it simple for you. If you want to find out more or see how our programs can help you, just get in touch. We offer a free estimate with no obligation.

For additional information on how to get out of a title loan and get more money, check out our helpful guide here. This guide will show you options to access extra cash and successfully pay off your title loan.

Contact us today online or by phone at 800-700-8900 to learn more.